February 2025

“Investing in an Era of U.S. Economic and Market Dominance”

In today’s interconnected economy, global diversification has long been a key strategy for investors navigating uncertainty and capitalizing on emerging opportunities. Despite the turbulence of the past decade — marked by a pandemic, inflationary pressures and geopolitical disruptions — one fact remains clear: the United States has solidified its position as the powerhouse of global markets.

Three defining trends illustrate this dominance:

The U.S. economy continues to drive global growth, even as other major economies face headwinds.

The world’s largest companies are increasingly U.S.-based, particularly in the technology sector.

The U.S. stock market is becoming more concentrated, with fewer companies commanding a greater share of total market capitalization.

These trends are shaping the landscape for investors, businesses and policymakers. Navigating the risk and potential they create is critical in making strategic investments in the years ahead. While U.S. economic strength underpins global stability, an unprecedented concentration of market power introduces new vulnerabilities. Though a more evenly distributed global economy could mitigate these risks, the U.S. continues to play a pivotal role in shaping the financial future.

The U.S. Economy: An Engine of Global Growth

Global economies have endured a series of shocks in recent years, from COVID-19 to rising geopolitical tensions, all while grappling with the delicate balance between inflation and interest rates. While prominent economies such as China and the European Union have struggled to adapt, the U.S. has demonstrated remarkable resilience.

The chart above projects 2.2% annual GDP growth for the U.S. between 2024 and 2028, making it one of the strongest economies in the world. In contrast, the U.K. is expected to grow at just 1.5%. This sustained expansion is fueled by consumer spending, technological innovation, a diversified economy, and a dynamic labor market. Even amid mounting government debt (with the U.S. Debt-to-GDP ratio expected to reach 123%), the American economy continues to prevail. Comparatively, Japan’s projected Debt-to-GDP ratio of 248.7% in 2025 highlights the U.S.’s relative fiscal strength.

Monetary policy has been a driving force in managing inflation and supporting long-term growth. The Federal Reserve’s data-driven approach to interest rates aims to keep economic volatility in check. The U.S. remains one of the most attractive investment destinations, but for how long and will it last?

Echoes of the 1980s: A Blueprint for Today’s Market?

The last time the U.S. dominated the global markets was during the 1980s oil boom — a period that ultimately ended in economic turmoil. While the decade began with rapid growth, an oil glut in the mid-80s triggered a 50% market crash as Saudi Arabia ramped up production to regain market share. Energy-dependent economies, including oil-rich U.S. states, entered recessions — leading to job losses, bankruptcies, and an eventual banking crisis.

By October 19, 1987, the Dow Jones Industrial Average plummeted 22.6% in a single day — still the worst one-day percentage decline in U.S. history. The oil collapse rippled through the financial system, destabilizing corporate earnings and instigating uncertainty in energy and emerging markets. While today’s economy is different, the impact of market concentration on inflation, interest rates, trade, and corporate earnings is a growing concern.

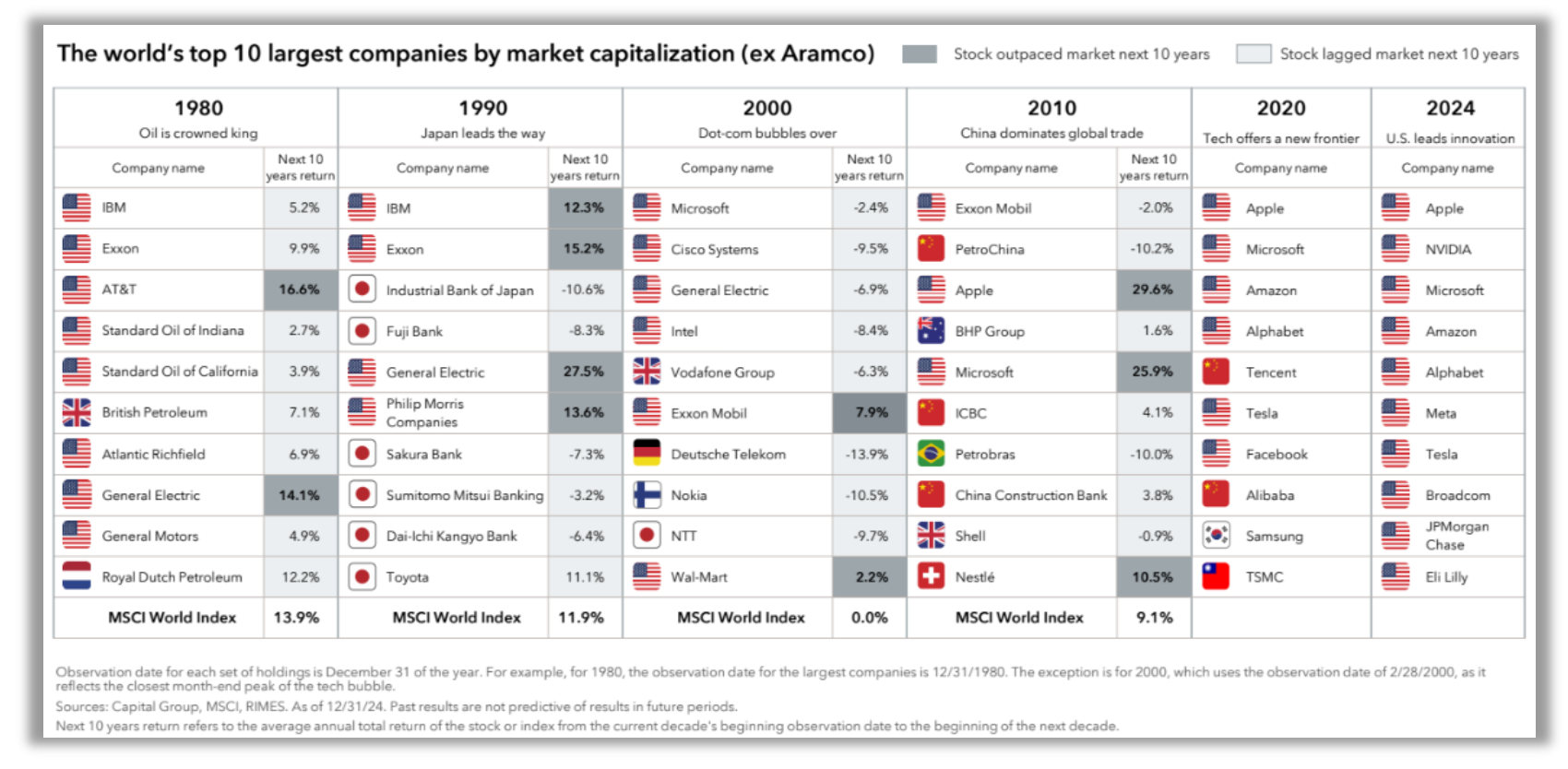

The top 10 global companies are now all U.S.-based, a testament to American innovation — but also a warning sign. Over-reliance on a limited number of companies could make the market more vulnerable to shocks, underscoring the importance of diversification. We saw previews of such shockwaves a few weeks ago. DeepSeek AI made its global debut, triggering a $400 billion plunge in Nvidia’s stock in just one day. DeepSeek claims its AI models achieve comparable power while using far less computational energy — at just $6 million. Investors fear that if DeepSeek can deliver high-performance AI at dramatically lower costs, demand for Nvidia’s premium chips could decline. As AI and chipmakers race to innovate, is Nvidia the most vulnerable to disruption? We've all heard the phrase "too big to fail," but are we entering an era of "too big to continue?”

The Rising Risks of Market Concentration

The U.S. stock market is becoming increasingly top-heavy, with fewer companies controlling a greater share of total market capitalization than ever before.

In March 2000, the top 10 companies in the S&P 500 made up 26.6% of the index’s market cap. By December 2023, that figure had surged to 37.34%, highlighting the growing influence of a small group of corporations. By contrast, the MSCI EAFE Index, which tracks developed markets outside the U.S. and Canada, is far more diversified. The top 10 companies in that index account for just 13.69% of its total market cap, reducing systemic risks.

Historically, highly concentrated markets have seen greater volatility, threatening the long-term health of global equities. The previous peak in S&P 500 concentration occurred during the 2000 dot-com bubble at 26.6% when a handful of tech giants led the market to unsustainable heights before a dramatic collapse. Today, we may be witnessing a similar pattern.

The Case for Caution with the Mag 7

The Magnificent 7 — Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla — have been the primary engines of U.S. market growth. They currently make up over 30% of the S&P 500. In 2024, they accounted for more than 50% of the index’s total gains. But what happens if the Mag 7 falters?

The Mag 7 contains the world's most powerful yet the most scrutinized companies. Governments worldwide are tightening regulations on big tech, focusing on antitrust laws, data privacy, and AI policy. Stricter oversight could stifle innovation.

While the Trump administration is anticipated to offer deregulation and tax cuts to mega-cap tech companies, other policies could spur geopolitical disruption. Trade policies and tariffs — particularly involving China — could hinder supply chains and limit U.S. tech expansion. A level of uncertainty surrounds the Mag 7’s earnings. Tesla’s revenue has missed expectations and Meta’s stock trades at 28 times projected 2025 earnings — a valuation that could prove precarious if growth slows.

Optimistically, when we take the Mag 7 out of the equation, what we have is stable, healthy growth – not too different from other leading international markets. In late 2023, the Mag 7 saw a sharp rise in earnings, followed by a significant decline. With growth stocks particularly sensitive to interest rates, if the Federal Reserve keeps rates high or delays cuts, it could pressure these stocks further.

History shows that high-flying tech stocks don’t stay invincible forever. If the Magnificent 7 struggle, the broader market could suffer the consequences.

Conquer or Crash? What’s Next for Investors?

As we move through 2025, market volatility is activated by shifting economic indicators and political unpredictability. Consumer confidence is declining with rising inflation expectations influencing cautious spending behaviors. The services sector is contracting, signaling potential headwinds. Stagflation fears are building, with inflation persisting and trade restrictions tightening from China, Canada and Mexico. Efforts to deregulate finance and energy are underway – however, these changes have elicited mixed reactions, leading to debates about their long-term impact. Since January, European markets have been outperforming the S&P 500 for the first time in a decade – a trend that investors should monitor closely. Could this signal a shift in global market dominance?

The Path Forward

Given Europe’s underperformance for the last decade, there are some advisors who have been reluctant to add international exposure to their portfolios. And for those advisors, their strategies have likely performed very well for the last decade or more. But anyone can buy and hold the Mag 7 and look like a genius…for now. For investors, diversification is – and will continue to be – paramount. The U.S remains at the forefront of tech, manufacturing, industrial, and healthcare. Beyond the usual suspects, mid-cap stocks (SMIDs) offer opportunities for high-yield returns and emerging performers that may not yet have mass appeal. The Magnificent 7 didn’t start as giants – new leaders will emerge as markets evolve. Strategic investing isn’t about chasing trends — it’s about positioning for long-term success in an ever-changing economic landscape. Will the U.S. continue its reign or are we on the verge of another turning point? Only time will tell.